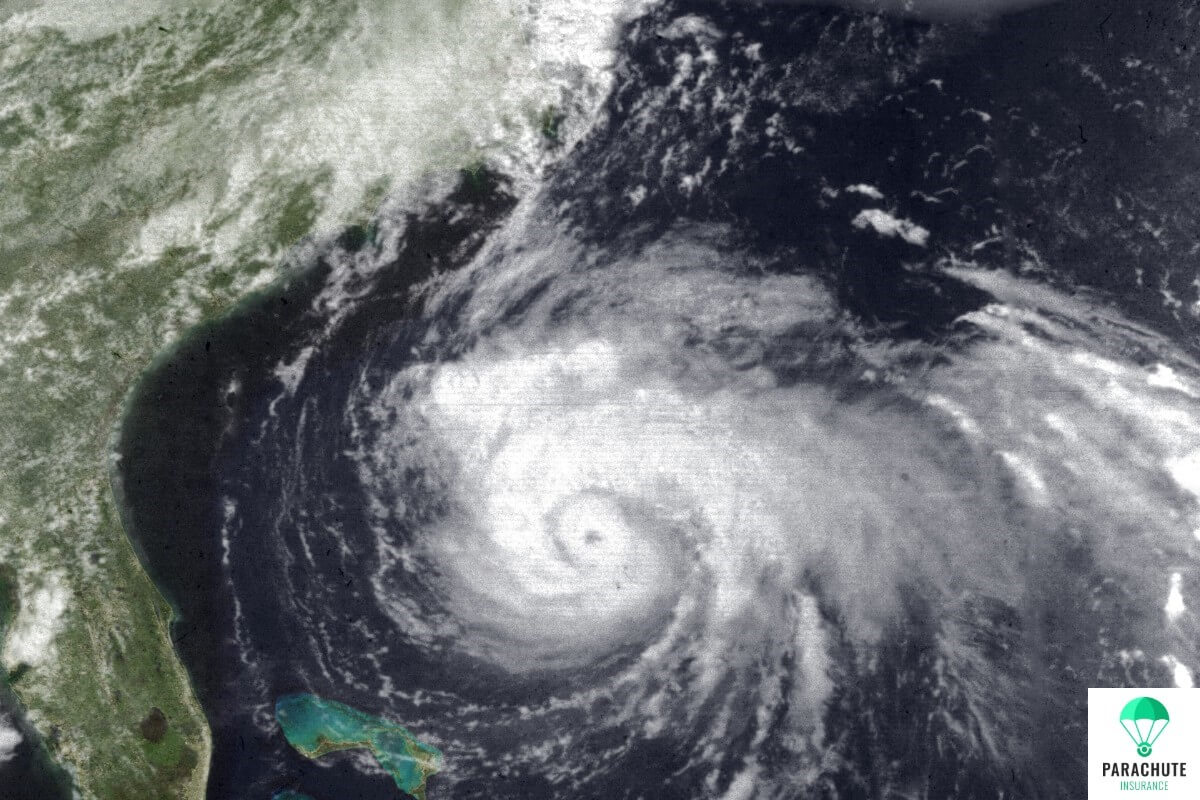

The 2020 Atlantic hurricane season was extremely active and broke many records:

- 30 named tropical storms – more than ever recorded and exceeding the alphabetical list of 21 Atlantic storm names.

- 12 tropical storms hit the U.S., of which 5 came ashore in Louisiana – 3 more than the previous record from 1916.

Tropical cyclones impacted the entire U.S. coastline from Texas to New Jersey last year but hit particularly hard the Caribbean and Central America. In this blog, we are taking a look back at the major hurricanes making U.S. landfall and what damages they caused before we share our perspective on how you can prepare for 2021.

The Storms

The 2020 Atlantic hurricane season produced 30 named tropical storms of which 12 made landfall in the U.S. The season got off to an unusual early start with tropical storm Arthur in mid-May, two weeks before the official start of hurricane season on June 1st. By July, three tropical storms, Edouard, Fay, and Gonzalo, broke the record for earliest fifth, sixth, and seventh named storms, respectively. Many more hurricanes and tropical storms formed over the summer. In the month of September, 10 tropical storms formed, more than in any month on record. By the end of October, hurricane Zeta became the 27th named storm of the season, the most since 2005, and the 11th storm to make landfall in the U.S. Eta was the last tropical storm impacting the US in 2020. It made landfall twice in Florida on November 8 and 12 after having steamrolled as major hurricane into Central America.

Tropical cyclones with maximum sustained winds of 39 mph or higher are called tropical storms (and receive a “name” from the National Hurricane Center). Storms with maximum sustained winds of 74 mph or higher are called hurricanes. They are categorized from 1 to 5 on the Saffir-Simpson Hurricane Wind Scale. The higher the wind speed, the higher the category, and the greater the hurricane’s potential for property damage.

Here is an overview of the most notable hurricanes (from a U.S. perspective):

- Hurricane Hanna: Category 1 Hurricane Hanna, the earliest 8th named storm on record, made landfall at Padre Island, Texas on July 25. High winds and heavy rainfall, up to 12 inches, caused widespread flooding in the Rio Grande Valley.

- Hurricane Isaias: Tropical storm Isaias brought high winds and heavy rain to Puerto Rico on July 29-30 before traveling north passing by the coast of Florida, Georgia and South Carolina. It intensified over the Atlantic and made landfall as a Category 1 hurricane near Ocean Isle Beach, North Carolina on August 3. High winds and heavy rains were experienced much further inland than normal reaching from Virginia all the way to New England. Millions of people lost power and 5 people died as a result of the hurricane.

- Hurricane Laura: On August 27, Hurricane Laura made landfall near Cameron, Louisiana as a Category 4 hurricane with sustained winds of 150 mph before downgrading to a Category 2. It tore off roofs while knocking out power to hundreds of thousands of people. A large storm surge occurred over much of Louisiana’s coastline and flooding rainfall extended into western and central Louisiana. Over 500,000 residents were evacuated. 98% of households in Cameron County lost power. At least 27 people were killed. The total economic losses are estimated at $16 billion.

- Hurricane Sally: Hurricane Sally made landfall near Gulf Shores, Alabama, as a Category 2 hurricane on September 16. Flooding along the Alabama-Florida border forced thousands of rescues. In Florida alone, Sally dumped four months of rain in four hours causing widespread flooding. Due to high winds and flooding, hurricane Sally left many communities heavily damaged in its wake.

- Hurricane Delta: On October 6, Hurricane Delta rapidly intensified from a tropical storm into a Category 4 hurricane over the Caribbean Sea putting much of the Gulf Coast, from Texas to Florida panhandle, on high alert. It eventually made landfall near Creole, Louisiana as a Category 2 hurricane, only 12 miles away from where hurricane Laura caused massive destructions only 6 weeks earlier. Four people died and nearly 150,000 people lost power. The hurricane also caused 10 tornadoes to develop causing additional damages.

- Hurricane Zeta: Category 2 Hurricane Zeta made landfall near Cocodrie, Louisiana on October 28 taking the lives of 6 people. The hurricane caused over 2 million people to lose power.

Visit here for a full breakdown of all the storms in the 2020 Atlantic hurricane season.

To watch a great visualization of all 2020 hurricanes and tropical storms, watch this clip produced by NASA.

The Impact

The total economic losses from hurricanes and tropical storms in the U.S. in 2020 are estimated to be $37 billion, ranking the eighth highest total on record. All while scientists are attributing an increasing frequency and intensity of hurricanes to the effects of climate change.

For families living near the Atlantic and Gulf of Mexico coasts, the threat of costly damages from hurricanes is a real concern. There is a large gap in standard home insurance coverage that leaves many families financially vulnerable. Standard insurance policies exclude damages from flooding and limit the insurer’s financial responsibility in the form of hurricane deductibles.

Looking Ahead

The reality is that standard homeowners insurance policies are not sufficient to protect families from the very real and increasing threat of hurricanes. One option to help fill this insurance gap is parametric insurance, a new form of insurance that offers quick and painless support in the immediate aftermath of a crisis. Parachute Insurance is designed to increase financial resilience for hurricanes and removes the need for an adjuster or a lengthy claims process. It pays homeowners emergency cash within hours after a hurricane hit.

The 2020 hurricane season was brutal, and the unfortunate reality is that the next hurricane season could be the same – or worse. We want you to be physically and financially prepared before the next hurricane hits so you can stay resilient to these storms!

Visit our blog to learn more about how you can increase your financial preparedness before the next hurricane.